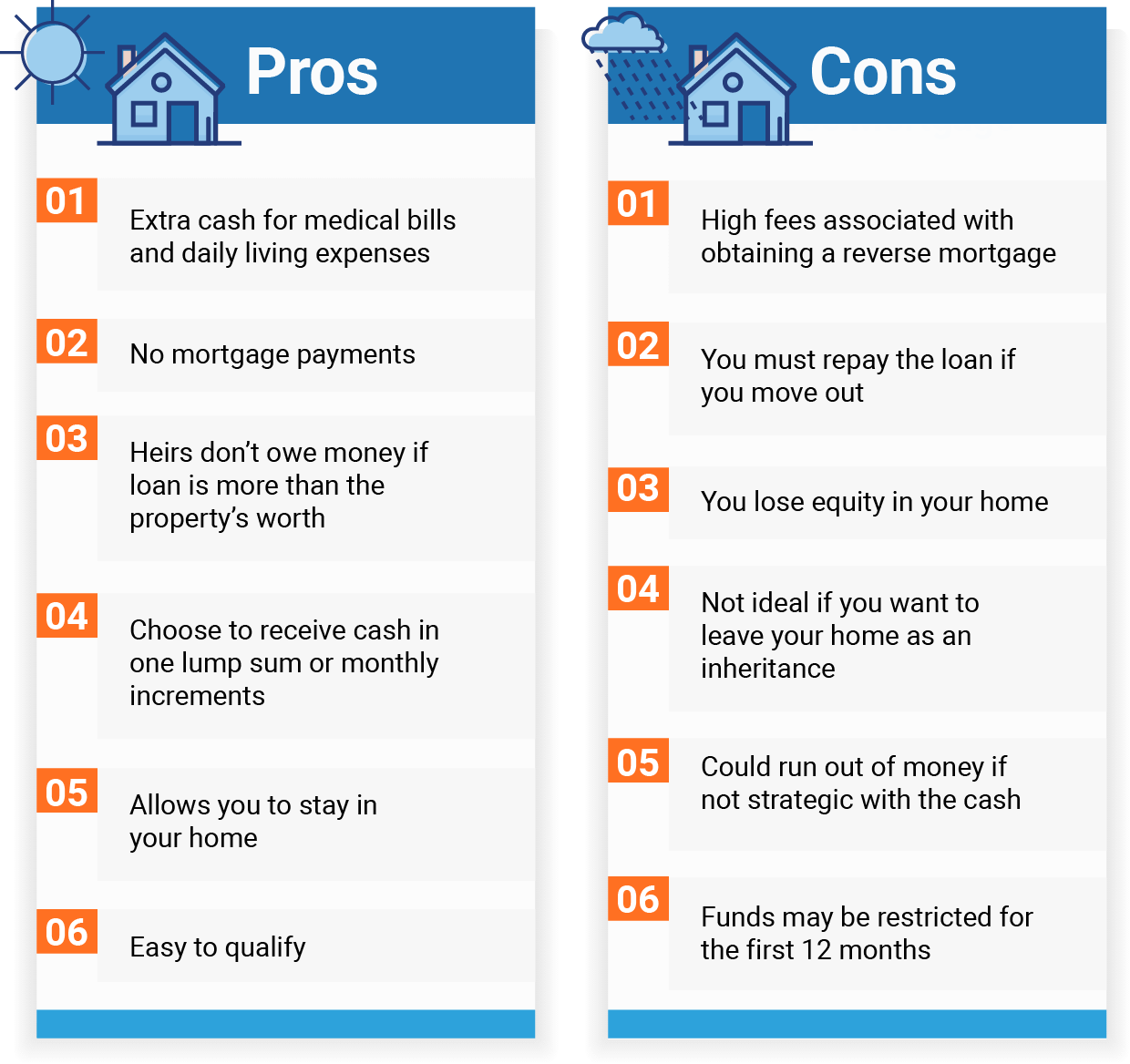

The FBI and the U.S. Department of Housing and Urban Development Office of Inspector General (HUD-OIG) desire consumers, particularly senior citizens, to be watchful when looking for reverse home loan products. Reverse home mortgages, also known as home equity conversion mortgages (HECM), have actually increased more than 1,300 percent between 1999 and 2008, producing considerable chances for fraud perpetrators. It likewise guarantees that, when the loan does become due and payable, you (or your successors) do not have to pay back more than the value of the house, even if the quantity due is higher than the evaluated value. While the closing expenses on a reverse home mortgage can sometimes be more than the costs of the house equity line of credit (HELOC), you do not need to make regular monthly payments to the lending institution with a reverse home loan.

It's never a great idea to make a monetary choice under tension. Waiting until a little problem becomes a big problem reduces your alternatives. If you wait up until you remain in a monetary crisis, a little additional earnings monthly probably hyatt timeshare won't help. Reverse home mortgages are best used as part of a sound monetary plan, not as a crisis management tool.

Discover if you may get approved for help with expenditures such as property taxes, home energy, meals, and medications at BenefitsCheckUp. Reverse home loans are best used as part of a total retirement strategy, and not when there is a pending crisis. When HECMs were very first used by the Department of Real Estate and Urban Advancement (HUD), a large percentage of borrowers were older females looking to supplement their modest earnings.

During the housing boom, lots of older couples took out reverse home mortgages to have a fund for emergency situations and extra money to take pleasure in life. In today's economic recession, younger debtors (typically Baby Boomers) are turning to these loans to handle their existing home loan or to help pay for debt. Reverse mortgages are special due to the fact that the age of the youngest borrower figures out how much you can borrow.

The Facts About What Is Today Interest Rate For Mortgages Uncovered

Choosing whether to secure a reverse home mortgage loan is challenging. It's tough to approximate for how long you'll remain in your house and what you'll require to live there over the long term. Federal law requires that all individuals who are thinking about a HECM reverse mortgage get counseling by a HUD-approved therapy firm.

They get rid of timeshare will also go over other choices including public and personal benefits that https://www.deviantart.com/thothesvtk/journal/Fascination-About-What-Is-Home-Equity-Conversion-M-874675378 can help you stay independent longer. It's valuable to consult with a therapist prior to speaking to a loan provider, so you get impartial details about the loan. Telephone-based counseling is offered nationwide, and face-to-face counseling is readily available in numerous communities.

You can likewise discover a therapist in your location at the HUD HECM Counselor Roster. It is possible for reverse home mortgage debtors to deal with foreclosure if they do not pay their residential or commercial property taxes or insurance coverage, or keep their house in great repair work (how do mortgages work in canada). This is especially a risk for older homeowners who take the whole loan as a lump sum and spend it quicklyperhaps as a desperate effort to restore a bad scenario.

Nevertheless, starting in 2015, brand-new guidelines require that reverse home mortgage applicants undergo a lender financial evaluation at the time of application. This is similar to the underwriting process in a standard home mortgage. The lending institution will look at credit reports, payment history, and household financial obligation prior to starting a loan. That's why reverse home loan therapy is so important.

How Who Has The Best Interest Rates For Mortgages can Save You Time, Stress, and Money.

They will likewise take a look at your financial scenario more broadly to help you determine if a HECM is best for you. Always prevent any unsolicited deals for a reverse mortgage or for aid with these loans. If you believe you or your household have been targeted by a scammer, call 800-347-3735 to file a complaint with HUD.

When you first begin to discover about a reverse home mortgage and its associated advantages, your preliminary impression may be that the loan product is "too great to be real (who took over taylor bean and whitaker mortgages)." After all, an essential advantage to this loan, developed for homeowners age 62 and older, is that it does not require the customer to make monthly home mortgage payments.

Though in the beginning this advantage may make it appear as if there is no repayment of the loan at all, the reality is that a reverse home loan is just another type of house equity loan and does eventually get paid back. With that in mind, you may ask yourself: without a month-to-month home loan payment, when and how would repayment of a reverse home mortgage occur? A reverse home loan is various from other loan products because payment is not achieved through a monthly home loan payment with time.

Loan maturity usually takes place if you offer or transfer the title of your home or permanently leave the house. However, it may also occur if you default on the loan terms. You are considered to have completely left the home if you do not reside in it as your main home for more than 12 successive months.

The Best Guide To What Are Interest Rates Now For Mortgages

When any of these instances occur, the reverse mortgage ends up being due and payable. The most typical method of repayment is by offering the home, where earnings from the sale are then used to repay the reverse mortgage in complete. Either you or your beneficiaries would generally take responsibility for the deal and get any remaining equity in the house after the reverse home loan is paid back.

A HECM reverse mortgage makes sure that borrowers are just responsible for the amount their home offers for, even if the loan balance exceeds this amount. The insurance coverage, backed by the Federal Real Estate Administration (FHA), covers the remaining loan balance. In circumstances when successors choose to keep the house rather of selling it, they may choose another type of repayment.

Qualifying beneficiaries may likewise re-finance the home into another reverse home mortgage. A reverse home loan payoff isn't limited to these alternatives, however. If you would like to pay on the reverse home loan during the life of the loan, you definitely might do so without penalty. And, when making regular monthly home loan payments, an amortization schedule can prove beneficial.