If that ratio of yours isn't beneficial, settle existing financial obligation or shot enhancing your income with a 2nd job. Finally, you'll require to put some cash towards the purchase of your house, the amount of https://lorenzoaudg902.wordpress.com/2021/02/17/the-only-guide-to-what-is-the-current-rate-for-home-mortgages/ which will depend on the kind of mortgage you get. Usually speaking, you'll require a 20% deposit when you take out a traditional loan to prevent personal home loan insurance coverage, or PMI.

It generally gets added on to your month-to-month home loan payment and equals 0. 5% to 1% of the amount of your home loan. For example, with a $150,000 home loan, you'll typically be taking a look at $750 to $1,500 in PMI every year, expanded over 12 months.

I was speaking to my 16-year-old kid recently, and he had some concerns. Like. What is a mortgage? What does your credit rating require to be? How do they work?Many people today are uninformed when it comes to purchasing a home and how all of it works. In this short article, we break down what a home loan is and how it works from start to complete for the novice.

Some Ideas on Why Are Reverse Mortgages A Bad Idea You Need To Know

When you buy a house, for the most part, you will be needed to use a down payment, normally in between 3. 5% -20% of the purchase rate you will pay rci timeshare cost in cash. The remaining quantity is borrowed from a home loan lending institution; this loan is called a home loan. For instance, You make an offer of $200,000 on a home, and it is accepted.

You will need a loan from a home mortgage loan provider for the staying 90% ($ 180,000). Once the sale is complete, you now have a $180,000 home loan to make monthly payments to the lender.FHA loans are popular with novice property buyers since they require simply a 580 credit score with a 3.

Fannie Mae and Freddie Mac developed the Conventional 97 loan program, which requires just a 3% down payment. They are harder to receive, requiring a 680 credit report. Fannie Mae and Freddie Mac produced the HomeReady and House Possible loan program to complete with low down payment mortgage such as FHA loans.

Getting My How Do Banks Make Money On Reverse Mortgages To Work

A traditional home mortgage is not backed by the Government and fulfills the requirements of Fannie Mae and Freddie Mac, the 2 largest buyers of home mortgage. Veterans of Extra resources the U.S. military are eligible for a VA loan, which needs no down payment or home loan insurance.USDA loans are for low-to-median income property buyers in rural parts of the country. 35%. When you get a home mortgage loan, there are more things to pay besides simply the principal balance and interest. There are taxes, insurance, and HOA fees to pay. Here is a breakdown of all the expenses connected with a house loan. The principal balance is the amount of money you obtained. For the very first couple of years, just a small amount of your home mortgage payment goes to the principal; as the loan goes on, a bigger percentage goes to the primary balance. Every state in the U.S. has real estate tax that will be due each year. The county will assess the value of your home and charge you based upon the county tax rate. The lending institution will make the tax payment when it ends up being due.Private mortgage insurance (PMI )is insurance coverage on the loan itself. If a customer defaults on the loan, the insurance coverage business will reimburse the home mortgage loan provider. PMI is needed on all conventional loans with a loan-to-value ratio higher than 80 %. Suggesting unless you put down at least 20%, you will be needed to carry home loan insurance. FHA MIP rates differ based on the amount of your downpayment.VA loans do not need the customer to bring mortgage insurance coverage at all.Closing expenses are charges charged by the home mortgage business for funding and processing the loan. You will be charged for products such as your credit report( $20-$ 35), loan application charge ($ 200-$ 400), and a loan origination fee (2% -5 %of the sales rate). This will guarantee you're getting a competitive interest rate and closing expenses. The most typical loan term is a 30-year fixed-rate mortgage.

A fixed-rate loan is where you lock in your rate of interest for the entire term. 15-year fixed-rate home mortgages are also a popular alternative for those desiring a lower interest rate and paying off their loan in half the time. The most typical is a 5/1 ARM, where the first five years of the loan you have a low-interest rate, then the rate increases every year.

This is a excellent alternative for homebuyers who do not plan on staying in the house for at least 5 years. Now that you know what a mortgage is, you most likely wish to know what you need to qualify for a home loan. Your earnings requires to be sufficient to afford the loan. Lenders will accept not all kinds of earnings; earnings must correspond and reliable. If you are a 1099.

What Are The Best Interest Rates On Mortgages for Beginners

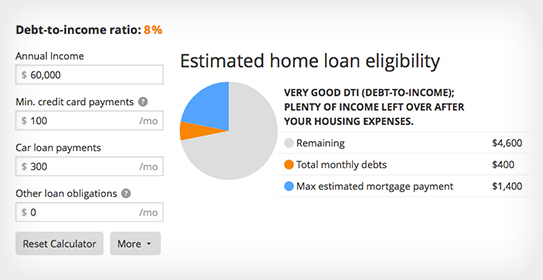

worker paid commissions or by the task, the lender will require two complete years of tax returns. They will take the typical earnings you have made in the last 2 years to use as your earnings. For example, if your monthly income is$ 5,000 each month, and you have a$ 200 credit card payment,$ 400 automobile payment, and your projected home loan payment is$ 1400.

The total financial obligation payments are $2,000, which is 40% of your earnings. Lenders like to see an optimum DTI ratio of 36 %but may permit approximately 45 %in some cases - how many mortgages are there in the us. A down payment is a percentage of the purchase rate a debtor requires to pay in money at closing. The amount you require to have down will depend.

on the kind of home loan you get.FHA loans only require a 3. 5% down payment, while a traditional loan will require in between 5% -20 %down. One of the biggest elements in determining your eligibility for a home loan is your credit report. For many mortgage, you will need a 640 credit report.

Unknown Facts About How Do Reverse Mortgages Work?

However, some lenders may have the ability to accept lower credit rating for an FHA loan. FHA loans need a 580 credit report with a 3 - who took over taylor bean and whitaker mortgages. If you have a credit history of 500-579, you may qualify with a 10% down payment. Nevertheless, finding a lending institution that will work with ratings under 580 will be difficult.

If your score is below 580, you must enhance your score prior to requesting a mortgage. Have a look at our tips for raising your credit history fast. Make certain you work with an experienced property agent and loan officer who can stroll you through the house purchasing procedure from start to complete. Do you believe you're prepared to get a mortgage?. A home loan, generally speaking, is a loan. When you set out to buy a home, no one anticipates you to have, state,$ 500,000 in money. So that's where a mortgage is available in: You obtain the money that you need to buy your selected house, accepting pay it back in the coming years.